TJ Chambers

Apparently, Bruno Mars now holds the record for the largest single-day ticket sales for the promoter Live Nation, with 2.1 million sold for ‘The Romantic Tour’ across North America, Europe and the UK with currently 77 events via Ticketmaster plus another two via Paciolan (at the Falcon Stadium – USAF Academy, Colorado Springs).

The promotional press released by Live Nation enthusiastically gushed: Bruno Mars shatters records with ‘The Romantic Tour’, stating:

Making History

The Romantic Tour made history with the largest single day ticket sales in Live Nation history across North America, Europe, and the UK.

Breaking Records

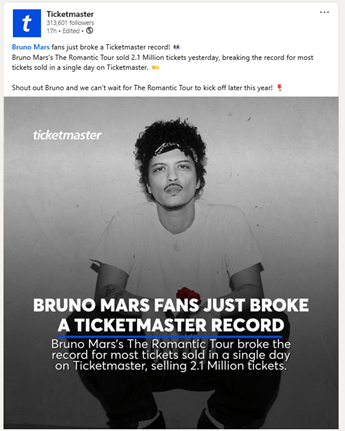

The tour set a new Ticketmaster record for the most tickets sold in a single day, with 2.1 million tickets moved.

A Major Comeback

Bruno Mars’ first ever full stadium tour now spans 70 shows across North America, Europe, and the UK, marking his first full headline tour in nearly a decade following the record breaking 24K Magic World Tour.

All wonderful self-congratulatory stuff, but perhaps the second point is open to misinterpretation, stating it’s ‘a new Ticketmaster record for the most tickets sold in a single day’, rather than ‘the most tickets sold in a single day, for a single artist, as promoted by Live Nation’ – which obviously doesn’t roll-off-the-tongue as easily.

So maybe a little misleading. Or even incorrect – but more on that shortly.

Not that the music industry media had any doubts, for example Pollstar stated:

‘The global superstar set a single-day ticket sales record for Live Nation across North America, Europe and the U.K.’, fine so far, but then continued ‘and he also shattered a Ticketmaster record by moving 2.1 million tickets in a single day.’ (Bruno Mars Shatters Ticket Sales Records With Unprecedented Demand for ‘The Romantic Tour’, Oscar Areliz, 16.01.26 – https://news.pollstar.com/2026/01/16/bruno-mars-shatters-ticket-sales-records-with-unprecedented-demand-for-the-romantic-tour/).

Similarly, Music Business Worldwide shared: ‘The on-sale also set a new Ticketmaster record for the most tickets sold in a single day.’ (Bruno Mars breaks Ticketmaster single-day sales record, with 2.1m tickets sold for ‘The Romantic Tour’, Mandy Dalugdug, 19.01.26 – https://www.musicbusinessworldwide.com/bruno-mars-breaks-ticketmaster-single-day-sales-record-with-2-1m-tickets-sold-for-the-romantic-tour/).

And MusicTalkers, reported, ‘…while Ticketmaster confirmed a new platform record of 2.1 million tickets sold in a single day.’ (Bruno Mars’ The Romantic Tour Sets Ticketmaster and Live Nation Records, Selling 2.1 Million Tickets in a Single Day, Andrew Braithwaite, 16.01.26 – https://musictalkers.com/latest-news/10078-bruno-mars%E2%80%99-the-romantic-tour-sets-ticketmaster-and-live-nation-records,-selling-2-1-million-tickets-in-a-single-day).

But why should the music media notice anything wrong when Ticketmaster itself published the following statement:

(c) Ticketmaster: https://www.linkedin.com/posts/ticketmaster_bruno-mars-fans-just-broke-a-ticketmaster-activity-7417710597137539073-DE0Y

Memory is fragile

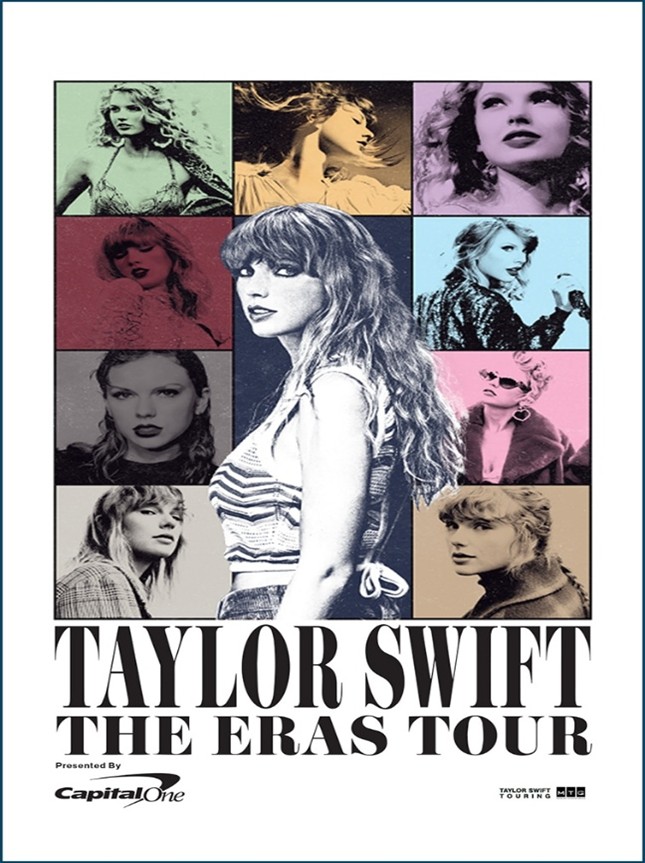

And just what is the problem with stating that ‘Bruno Mars fans just broke a Ticketmaster record’, well that’s because on the 15th November 2022, there was the initial onsale for Taylor Swift’s ‘Eras Tour’ – you may remember it as that led to no little debate about the robustness of Ticketmaster’s ticketing platform and the alleged antitrust behaviour of its parent Live Nation with subsequent Senate hearings (Hearing on Ticketmaster Sale For Taylor Swift Concert, 24.01.23 – https://www.c-span.org/program/senate-committee/hearing-on-ticketmaster-sale-for-taylor-swift-concert/622907), the DOJ (Justice Department Sues Live Nation-Ticketmaster for Monopolizing Markets Across the Live Concert Industry, 23.05.24 – https://www.justice.gov/archives/opa/pr/justice-department-sues-live-nation-ticketmaster-monopolizing-markets-across-live-concert) and FTC (FTC Sues Live Nation and Ticketmaster for Engaging in Illegal Ticket Resale Tactics and Deceiving Artists and Consumers about Price and Ticket Limits, 18.09.25 – https://www.ftc.gov/news-events/news/press-releases/2025/09/ftc-sues-live-nation-ticketmaster-engaging-illegal-ticket-resale-tactics-deceiving-artists-consumers) investigations into technical capabilities and market competitiveness etc.

As Ticketmaster itself explained in an extensive debrief / mea culpa (Taylor Swift | The Eras Tour Onsale Explained, 19.11.22 – https://business.ticketmaster.com/press-release/taylor-swift-the-eras-tour-onsale-explained/), over 3.5 million people pre-registered for Taylor Swift tickets, with 1.5 million sent Verified Fan codes and 2 million others held in reserve as Ticketmaster claimed typically customers buy an average three-tickets per transaction.

It however then admitted,‘Historically, we’ve been able to manage huge volume coming into the site to shop for tickets … However, this time the staggering number of bot attacks as well as fans who didn’t have codes drove unprecedented traffic on our site, resulting in 3.5 billion total system requests – 4x our previous peak.’

(c) Ticketmaster

Ticketmaster further claimed, ‘Over 2 million tickets were sold on Ticketmaster for Taylor Swift | The Eras Tour on Nov. 15 – the most tickets ever sold for an artist in a single day.’

Additionally, another 400,000 tickets were successfully sold via Capital One (Capital One Announces Exclusive Taylor Swift Tour Presale –https://www.capitalone.com/about/newsroom/taylor-swift-the-eras-tour-presale/) to their eligible cardholders in a separate pre-sale also powered by Ticketmaster, who additionally managed to retail another 1.1 million tickets for 3rd Party events in the US that same day, despite the frustrating system outages and disappointment for some consumers unable to acquire ‘Eras Tour’ tickets.

© Capital One / Taylor Swift / Eras Tour

This was separately confirmed by Michael Rapino who stated, ‘We sold two million tickets, the most we’ve ever sold in one day in history, and another million tickets of other artists on the same day. So, although we regret it was a slowdown in some queues and some error codes for a short period for some fans, we did manage to recover.’ (Taylor Swift Tour: Live Nation CEO Says “Everybody Crashed the Door” During Presale, Caitlin Huston, 17.11.22 – https://www.hollywoodreporter.com/business/business-news/taylor-swift-tour-tickets-pre-sale-1235264178/ )

So, Ticketmaster apparently sold over 2 million tickets for Taylor Swift, or 2.4 million tickets if you include the Capital One pre-sale, versus 2.1 million for Bruno Mars.

And obviously any confusion over best-ever single-day ticket sales for a single artist has nothing to do with the promoter of Taylor Swift being the Messina Touring Group / AEG, as opposed to Bruno Mars via Live Nation.

Ultimately, regardless of the total tickets sold, the platform does appear to have withstood the demands of the onsale better than in 2022 – notable if only because it attracted little critical comment from any frustrated media, politicos or ticket-buyers.

***

The John F. Kennedy Center

And in other news …. in February 2025, shortly after retaking office on his ‘Truth’ social media site President Trump stated, ‘At my direction, we are going to make the Kennedy Center in Washington D.C., GREAT AGAIN. I have decided to immediately terminate multiple individuals from the Board of Trustees, including the Chairman, who do not share our Vision for a Golden Age in Arts and Culture.’

Deborah F. Rutter had been the president of the Kennedy Center from 2014 to 2025, but was replaced by Trump’s longtime loyalist, and envoy for special missions, Richard Grenell, whilst also announcing himself as Chairman as he complained about ‘woke’ programming and ‘drag shows’ performed at the venue.

***

[In the U.K. we don’t really understand the outrage about ‘drag-shows’, but maybe that’s because the nation annually attends Xmas Pantomime. For overseas readers that is a type of musical comedy designed for family entertainment, typically combining bawdy humour, politics, singlalong pop tunes, and cross-dressing, all more or less based on a fairy tale. And they are massively popular.

And separately, the early development of punk in Manchester may have been different without the safe-harbour provided by Foo Foo Lammar and ‘The Ranch’ etc. Know your history.]

***

More insightful and professional commentators have noted that the attack on ‘woke culture’ is all part of the Trumpian erasure of diverse perspectives in art, literature, the media, and political discourse, with any dissent expressed to the increasingly authoritarian regime excluded from public platforms, censured by the use of multi-billion dollar lawsuits, and protected by a rigged judiciary, whilst activists, economic migrants, or foreign students are increasingly threatened with deportation from the country, and ‘democratic’ cities are subjected to roaming paramilitary ‘death squads’. (See: Bruce Springsteen ‘Streets of Minneapolis – https://www.youtube.com/watch?v=wWKSoxG1K7w)

The new hand-picked Kennedy Center board of Trump allies, underlings and friends included the White House deputy chief of staff for national security Dan Scavino; the White House chief of staff Susie Wiles; Wiles’ mother Cheri Summerall; Pamela Gross, who is a former adviser to Melania Trump; Usha Vance the wife of his vice-president J.D. Vance; White House director of presidential personnel Sergio Gor; Elaine Chao, Trump’s former labour secretary and the wife of Republican Sen. Mitch McConnell; Trump donor Patricia Duggan; Emily May Fanjul, wife of Trump donor and sugar magnate Pepe Fanjul; Dr. Dana Blumberg the wife of New England Patriots CEO Robert Kraft; and Mindy Levine wife of New York Yankees President Randy Levine.

The staff redundancies and changes to programming to reflect the new Trump cultural priorities that followed had an immediate effect.

In October a Washington Post analysis of ticketing data (https://www.washingtonpost.com/entertainment/2025/10/31/kennedy-center-sales/) found that sales for the three largest performance venues at the Kennedy Center – the Opera House, the Concert Hall, and the Eisenhower Theater – were the worst they had been since the pandemic.

The number of events were also impacted by a growing number of artists who withdrew from performing at the Center due to Trump’s involvement and the roll-back of diversity, equity and inclusion initiatives. This led to Richard Grenell claiming that CNN and The Washington Post (‘The legacy media are left wing activists – and they are open about it.’) were encouraging a boycott of the Center and threatened artists with legal action for cancelling their performances.

In December 2025 the institution was renamed The Donald J. Trump and The John F. Kennedy Memorial Center for the Performing Arts, as the new board voted unanimously to make the change due to ‘the unbelievable work President Trump has done over the last year in saving the building’.

Since then, many artists have cancelled their appearances at the Centre, including, Renée Fleming, the Washington National Opera, Vocal Arts DC, Seattle Children’s Theatre, Sonia De Los Santos, Martha Graham Dance Company, Béla Fleck, Issa Rae, Kristy Lee, Wayne Tucker, Brentano Quartet with Hsin-Yun Huang, Magpie, Doug Varone and Dancers, the comedy show ‘Asian AF’, the touring production of ‘Hamilton’, Chuck Redd, The Cookers, Stephen Schwartz, Rhiannon Giddens, Balún, Issa Rae, and most recently Philip Glass.

(c) Philip Glass / X: https://x.com/philipglass/status/2016179940815761860

While the resignations and departures continue, with Kevin Couch the VP of Artistic Planning stepping down after only two-weeks in post, and Sarah Kramer, the Senior Director of Artistic Operations fired after a decade in post – More staff shakeups at the Kennedy Center, Anastasia Tsioulcas + Elizabeth Blair, 29th January 2026 – https://www.npr.org/2026/01/29/nx-s1-5692872/kennedy-center-resignation.

A Man Is Known by the Company He Keeps

It’s an old saying that a man is known by the company he keeps. But similarly, a company is also known by whom they appoint to their board.

In May 2025, Live Nation appointed Richard Grenell to its Board of Directors, with the company stating, ‘Mr. Grenell brings decades of experience in diplomacy and negotiations, having served as U.S. Ambassador to Germany, Acting Director of National Intelligence, Presidential Envoy for Kosovo-Serbia Negotiations and Presidential Envoy for Special Missions.’ (Live Nation Entertainment Elects Richard Grenell to Board of Directors, 20.05.25 – https://newsroom.livenation.com/news/live-nation-entertainment-elects-richard-grenell-to-board-of-directors/).

A number of film studios, talent agencies and others especially those considering major acquisitions, have enlisted lobbying firms and/or individuals that have connections to the Trump administration (for example Trey Gowdy who successfully convinced President Trump to grant a ‘full and unconditional pardon’ to Tim Leiweke former CEO, Oak View Group despite the DOJ stating he was responsible for ‘orchestrating a conspiracy to rig the bidding process for an arena at a public university in Austin, Texas’), but Grenell’s hiring by Live Nation is different, as he is one of the president’s closest advisers.

The Hollywood Reporter covered the obvious self-interested nature of Grenell’s appointment, stating it was part of its campaign to squash the antitrust lawsuit Live Nation faces against the DOJ, quoting anonymised industry sources:

‘Right in front of our very eyes you’re watching a transaction take place where one group is trying to buy their way out of the DOJ and 40 state attorneys pursuing them’.

The article continued:

‘A second music executive, who requested anonymity citing fear of retaliation from Live Nation, called Grenell’s appointment “the most thinly-veiled attempt to clash a legal proceeding that I’ve seen.’

‘What expertise is he able to provide other than his access to Trump,’ the executive says. ‘What value does he provide? It’s just so obvious. if he wasn’t closely aligned with Trump, would they have ever picked him? If they didn’t have a lawsuit filed by the DOJ would they have appointed him? The answer to both is likely no.’

Music Insiders Slam Live Nation’s Trump Ally Board Appointee Amid DOJ Suit: “It’s Just So Obvious”, Ethan Millman, 21.05.25 – https://www.hollywoodreporter.com/business/business-news/live-nation-richard-grenell-doj-lawsuit-1236224658/

The United States District Court for the Southern District of New York (United States of America Vs. Live Nation Entertainment + Ticketmaster LLC) has a tentative trial start date of 2nd March 2026.

Until next time.