TJ Chambers

© VectorStock.com

I was enjoying a fine cappuccino made by barista Ollie in the Soho sunshine whilst video conferencing with a number of smart young people all of whom have day-jobs of some seniority, and they were of the collective opinion that the moment of peak-secondary ticketing had passed.

During the discussion, there was specific reference to the recent revenue declines posted by the publicly listed major secondary marketplaces (raising concerns about their long-term viability), and the growing anti-tout lobby (for example: the FanFairAlliance, UK; FEAT (Fully-Authorised European Alliance for Ticketing); PRODISS, France; BDKV, Germany; AssoMusica, Italy; and others), together with consumer protection agencies (for example, Which? UK, and CHOICE, Australia) and the increased levels of regulatory oversight of unauthorised resale with a focus on drip-pricing, deceptive practises i.e. the verification of sellers and fraudulent listings (where virtual or actual supply-monetises-demand), and the need for (price-cap) protection of consumers from excessive profiteering.

Also debated was whether the increased adoption of LLMs, for example the integration of Open AI’s ChatGPTinto the ticketing ecosystem (for example, StubHub App Launches in OpenAI ChatGPT – One of the First Ticketing Platforms to Offer Discovery Experience, 22nd December 2025 – https://www.businesswire.com/news/home/20251218386583/en/StubHub-App-Launches-in-OpenAI-ChatGPT-One-of-the-First-Ticketing-Platforms-to-Offer-Discovery-Experience; SeatGeek Launches in ChatGPT, 31st March 2026 – https://seatgeek.com/press/SeatGeek%20Launches%20in%20ChatGPT: or, Ticketmaster Drives a New Era of AI-Powered Event Discovery with App in ChatGPT, 9th April 2026 – https://business.ticketmaster.com/ticketmaster-drives-a-new-era-of-ai-powered-event-discovery-with-app-in-chatgpt/) would disrupt the search engine monopoly of event ticket discovery, and thus who sells the ticket – interestingly with the leading resale platforms all announcing their integrations early.

Additionally, the growth of ‘ethical’ and/or price-capped white-label resale solutions, and the widespread adoption of yield management tools by event rights owners and their primary ticketing partners had all combined to squeeze speculative resale margins previously lost to scalpers / touts and their secondary marketplaces, whilst also making ‘resale’ a commodified ticket-tech function rather than a distinctively standalone business.

The primary sector has in effect adopted many of the practices of secondary, typically enabling P-2-P ticket exchange and/or resale, albeit at a cost and with some restrictions (for example, typically imposing a price floor i.e. unable to list below the original face value), either through in-house development or via preferred 3rd Party partnerships and/or technical integrations.

And the secondary market’s response has been to increasingly compete for inventory access by incentivising official / primary engagement.

In effect, there is no longer any separation between the ‘primary’ and ‘secondary’ markets, but rather there is now a single ticketing marketplace which offers:

Pre-Sale – to closed-user groups whether fan clubs, supporter groups, preferred banking / mobile phone partners, or other commercial affiliates and sponsors, loyalty and/or membership schemes

On-Sale – the typically messy public distribution of tickets, where, at least for tier #1 artists and attractions, demand-oft-exceeds-supply with associated queuing and/or platform overload, fraud, and identity verification issues etc.

Up-Sale – Bundles (Ticket + Merchandise) & Packages (Ticket + Travel and/or Accommodation), Hospitality, Premium Experience, VIP, and other ‘value-add’ ticket inventory

and, Re-Sale – Revenue Optimisation by ticket-type & Dynamic (Surge) Pricing

A post by Dave Wakeman was also referenced in the discussion (The Secondary Ticket Market Is Free Falling … 28th April 2026 – https://davewakeman.com/2026/04/the-secondary-ticket-market-is-free-falling/), where he highlighted the downward movement in secondary ticketing activities, alongside recent regulatory fines and developing legislation.

***

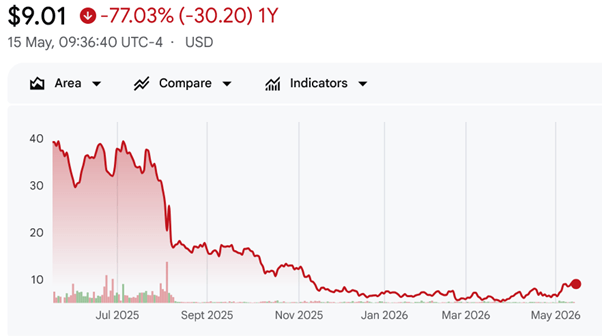

StubHub Holdings

© Google Finance

VividSeats

© Google Finance

***

So, is the resetting of ticket resale company valuations a temporary blip, or indicative of a potentially terminal decline of these marketplaces with their network of industrial-scale scalpers, bedroom touts, students-of-arbitrage, and others seeking to exploit the tension between excess demand and the limited (by event, game, concert, tour, or residency) supply of tickets.

Surely the post pandemic bounce-back of tours, tournaments and franchised festivals, coupled with the growing international network of theatres, arenas and stadia, have all combined to massively increase the scale, diversity and supply of global live entertainment, and thus the supply of ticket inventory.

Additionally, the widespread implementation of AI software – ‘bots’ – to acquire large quantities of tickets (with automated site scrapers, drop-checkers, fake account creation / account takeover, ticket spinners, card cracking, and price comparison as standard) and the widespread malpractice of ‘speculative listings’, has made the inventory acquisition and (re) listing process for resellers arguably easier than ever before.

The resultant hyper-inflated prices charged for in-demand ticketing provides the secondary marketplaces with sufficient margins for premium search engine placings (often above the original event rights owners ‘organic’ results), social media and offline advertising, and the utilisation of fiscal incentives, whether via commercial partnership, sponsorship and/or a revenue-split on the lift in ticketing GTV, to primary ticket inventory owners to consider alternate distribution channels – what viagogo / StubHub calls ‘Direct Issuance’.

But if the decline is real, what has changed to cause this apparent reversal of fortunes of these bullish marketplaces.

And when did this turnaround start.

***

(Not) Sold Out

Once upon a time (2016), Michael Rapino, the CEO, Live Nation Entertainment, was in conversation with Greg Parmley at ILMC #28 in a conference session entitled ‘Go Elsewhere for Tickets If You Missed the Onsale’, during which he stated that for the previous decade primary ticket agencies had publicly signalled when their allocation was ‘sold out’.

This had the unintended consequence that would-be ticket-buyers who missed the pre-sale or on-sale notification or event marketing message(s), were then inadvertently directed to the unauthorised secondary markets.

In effect, the primary platforms were educating its audience to find tickets elsewhere.

That the ‘sold out’ signposting was shaping consumer behaviour to the extent that they looked first to the secondary marketplaces, where tickets always ‘appeared’ to be available. Albeit often at an inflated price – but who knows the original ticket face value?

Rapino further explained to the ILMC that in order to (retrain) retain that audience, and recoup revenues otherwise lost to the secondary marketplaces, Ticketmaster+ an official ticket resale and exchange solution had been launched, and in the previous year Ticketmaster’s secondary revenues had grown 34% Y-O-Y, generating a GTV of $1.2Bn, at a time when the global secondary market was estimated to be approximately $8Bn.

Michael Rapino at ILMC #28 © IQ Magazine, 2016

Rapino continued that to ensure that revenues get to the event rights owners ticketing also needed to be priced correctly, and not less than its market value, stating ‘artists need to be braver in how they price the house’, otherwise revenues would continue to flow to the secondary companies.

But he admitted ‘that artists are still quite scared to charge high sums for front-row seats and less for those at the back’ as that wasn’t necessarily ‘a good brand position’ but argued that ‘the live business has had to fight fire with fire’.

Further, that the stance of artists not wanting to charge their fans too much was ‘honourable, but not realistic’.

***

‘If you spent $4,000 to buy a ticket, we should be kissing your ass!’

‘Referring to an article by Simon Jenkins in the London Evening Standard (http://www.standard.co.uk/comment/comment/simon-jenkins-how-making-tickets-cheaper-for-real-fans-is-a-gift-to-the-touts-a3192671.html), Rapino said: ‘Charge $4,000 for the front row and then take $3,500 and give it to charity. I’d rather the artist have the $4,000 to figure out how to subsidize your fans than thinking it’s worth $400 [while] someone else [is] making $3,600.’ (Live Nation’s Michael Rapino on Secondary Ticketing, 8th March 2016 – http://www.pollstar.com/news_article.aspx?ID=823278 – 404 Page Not Found)

***

A decade later, (2025), the message from Rapino hadn’t fundamentally changed. Concert tickets, especially in comparison with sports, were apparently still underpriced.

Michael Rapino © CNBC

Speaking at the CNBC Sport and Boardroom’s Game Plan conference, he stated: ‘In sports, I joke it’s like a badge of honour to spend [$70,000] for Knicks courtside. When you read about the ticket prices going up, it’s still an average concert price [of] $72. Try going to a Laker game for that, and there’s 80 of them [in a season].

(Live Nation CEO touts soaring demand, says concert tickets are still relatively underpriced, Luke Fontaine, 17th September 2025 – https://www.cnbc.com/2025/09/17/live-nation-ceo-demand-concert-tickets-underpriced.html)

***

Raising Grosses

Ticket pricing strategies employed by the more mercantile primary operators to increase show grosses for the event rights owners (whilst also attracting a margin for themselves), and to also reduce the revenue opportunity for the secondary market include:

Pricing-by-Date: Mid-Week versus Weekend

Pricing-by-Location: Stalls versus Balcony, ’Meet & Greet’, SoundcheckTix, Festival ‘Golden Circle’, capital versus regional dates

Pricing-by-Product: Ticket Bundles + Packaging, VIP + Hospitality

Timing: Early-Bird and/or Standby Pricing, Late-Sale Discounting, Walk-Up etc.

Variable Scaling: changing the configuration of an event auditorium between performances

Ticket Inventory Management: aka ‘slow ticketing’. Drip-feeding the amount of inventory available via adding shows or increasing allocations whilst ensuring ‘Demand (always) exceeds (available) Supply’. Can lead to fan / social media scare over unsold events and/or opaque ticket distribution policies

Demand (Surge) Pricing: flexible prices for tickets based on comparative secondary-market listings e.g. Ticketmaster’s ‘Platinum Tickets’. Albeit can lead to perception that artists are ‘scalping’ their own fans

There has also been a focus across live entertainment on the expansion of 3rd Party advertisers, affiliates, broadcast + media partnerships and sponsors, to increase revenues, whilst also amplifying event discovery, ticket distribution (through multiple branded pre-sale channels) and monetisation.

The resulting oft bewildering multitude of discrete but official pre-sales for the artist / promoter / venue / preferred credit card / tour sponsor / hospitality partner etc. also enables further variations on pricing as the ticket may represent only one (small) part of the actual cost of admission.

***

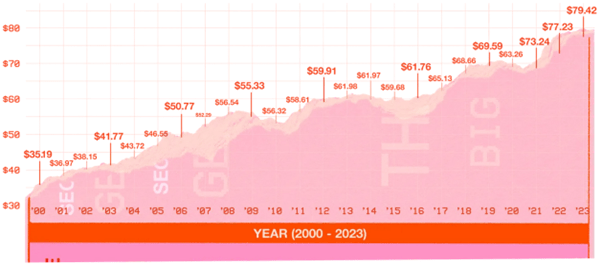

The Ever-Increasing Price of Tickets

Despite being written in 2023, a long-form essay in Pitchfork (The Price of Pop Fandom, Marc Hogan, Jill Mapes, and Marina Kozak, 3rd August 2023 – https://pitchfork.com/features/article/the-price-of-pop-fandom/)remains an illuminating piece of work with the following extract revealing the relentless above-inflation increase in the cost of the average worldwide concert tickets 2000 – 2023.

Source: Pollstar © Pitchfork

***

The Disruption of Secondary

As briefly mentioned earlier the secondary market has also been disrupted by new copy-cat entrants, some sector consolidation (for example: StubHub > Ticketbis > viagogo; Ticketmaster > TicketsNow > GetMeIn! > Seatwave; or VividSeats > Vegas.com > Wavedash (Japan) > Betcha Sports etc.) and a new generation of ‘ethical’ and/or face-value i.e. capped mark-up solutions.

These new platforms (for example, CashorTrade Ticketswap, Tixel, Twickets or Upfan etc.) typically partner with event rights owners to ensure ticket validity, adherence to price caps, and vet both sellers and listings. As a rule, these ‘authorised’ resale platforms don’t permit speculative listings and present themselves as an extension of the primary market.

Their added consumer value lies in restoring confidence to ticket-buyers who need resale flexibility without risking personal fraud or wanting to feed the ‘grey’ secondary market.

Primary (B-2-C) ticketing operators have also incorporated ‘closed-loop’ ticket exchange and/or resale services, for example, AXS Marketplace, CTS Eventim fanSALE, Ticketmaster Resale, etc. all designed to ensure traceability, compliance, and trust.

The increasing levels of digital securitisation / encryption technologies involved are also extending the various ‘gatekeeper’ controls of the original event rights owners, which irritates many secondary freemarketeers who see the ticket as a commodity, and not as a licence subject to various restrictive terms and conditions.

B-2-B ticketing platforms have also incorporated white-label ticket exchange and/or re-sale functionality for their clients including: menta tech, SeatGeek Enterprise, TrueTickets or vivenu etc.

In combination this has all served to part restrict the remit of the unauthorised secondary operators.

***

Future Prospects

If I was that clever, I’d have a proper job, but the future of (pure-play) secondary ticketing marketplaces is uncertain.

With declining stock prices, and thus lower market capitalisation and associated higher levels of vulnerability, increased competition from primary market solutions, and potential regulatory changes, these platforms must adapt quickly to survive in a challenging environment.

Not least because various industry reports suggest that the current global secondary market is currently valued at $2.09Bn (Business research Insights) to $3.41Bn (Source: Mordor Intelligence).

Of which North America accounts for approx. 41% with Europe including the UK approx. 28% market share.

Sporting events represents the largest segment of secondary ticketing with approx. 43% market share, and concerts 37%.

These overall secondary market valuations are considerably smaller than the previously quoted $8Bn 2016 estimate, which therefore arguably reveals the successful primary market penetration and conversion of secondary market activities.

Feel free to correct and/or update via the usual channels.

Until the next time.